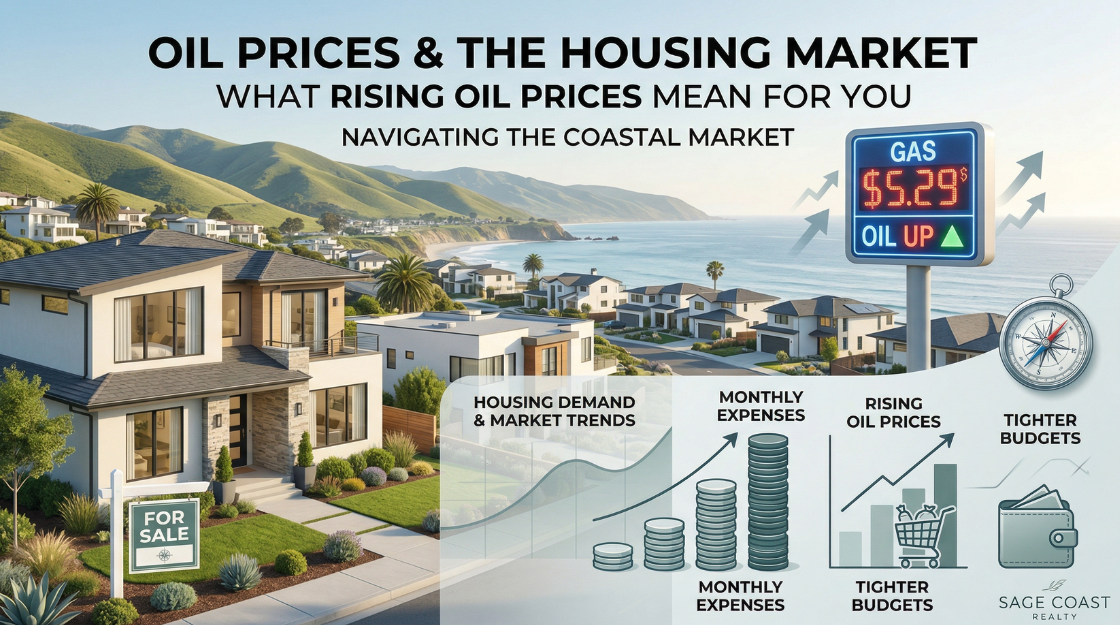

What Rising Oil Prices Mean for You and the Housing Market

You’ve probably noticed it already. Gas prices creeping up, headlines talking about oil, and a general feeling that things might be getting a little more expensive again.

So what does that actually mean for you… and for real estate?

Let’s take the emotion out of it and look at what’s really going on.

First, the obvious: everyday costs are going up

When oil prices rise, it doesn’t just affect what you pay at the pump. It touches almost everything, from groceries to shipping costs to services.

For most households, that creates a subtle but important shift. Monthly expenses increase, disposable income tightens, and financial decisions get more cautious. People may not panic, but they do start thinking twice.

How that mindset impacts homebuyers

Real estate is as much about confidence as it is about numbers.

When day-to-day costs rise, buyers become more conservative. They may lower their price range slightly, and decisions tend to take a little longer. It’s not that people stop buying; they just become more intentional.

Affordability doesn’t disappear… but it adjusts

Higher gas and living expenses don’t directly change mortgage payments, but they do affect how comfortable buyers feel with their overall budget.

A longer commute suddenly feels more expensive. Monthly ownership costs feel heavier. Buyers may start prioritizing practicality over stretching their budget. This can subtly shift what people are willing to pay, and where.

Location starts to matter even more

One of the biggest ripple effects we tend to see is a shift in location preferences. When fuel costs rise, proximity to work becomes more valuable, walkability and convenience gain importance, and long-distance commuting becomes less attractive.

This doesn’t mean outlying areas stop selling, but it can influence demand and pricing dynamics over time.

What sellers should know

If you’re thinking about selling, this is where strategy matters.

In a shifting environment, buyers become more selective. Pricing needs to reflect current conditions, not last month’s market. Homes that are well-prepared and well-priced still perform strongly. The market doesn’t stop; it just becomes more balanced.

The bigger picture

Rising oil prices can also influence the broader economy, including interest rates. Sometimes that leads to higher rates, and other times it slows the economy enough to bring rates down.

In other words, there isn’t a single guaranteed outcome, which is exactly why staying informed and not reactive is so important.

So… should you be worried?

Not necessarily.

What we’re seeing right now is not a sudden stop in the housing market. It’s more of a shift in behavior. Buyers are a bit more cautious, sellers need to be a bit more strategic, and the market becomes a little more thoughtful overall. In many ways, that’s a healthier environment than a frenzy.

Final thoughts

Markets evolve. That’s normal.

Rising oil prices are one of many factors that influence real estate, but they don’t define it. People still need to move, families still grow, and life doesn’t pause for economic headlines.

The key is understanding the moment we’re in and making smart, informed decisions within it. If you have questions about how any of this is impacting your specific situation, I’m always here to help you think it through.